Abstract

In 2023, stablecoins constitute over 40% of TVL in DeFi and are the most utilized assets across decentralized money markets. Numerous stablecoin projects, primarily decentralized ones, are launched every year and compete for greater market share.

Decentralized stablecoins emerge endlessly and evolve constantly because they serve as crypto-native assets and enjoy "Seigniorage" within their respective ecosystems, whose widespread applications promote interoperation and the growth of lending, staking, and other DeFi services based on them.

Building a comprehensive DeFi ecosystem is an aspirational goal for every decentralized stablecoin. The competition winner could expand their service offerings and enjoy the monopoly advantages of platforms.

Various stablecoin projects were developed or enhanced in this cycle to offer more decentralized and yield-bearing options. It's mainly because the biggest stablecoin issuer, Tether, has generated significant revenue but does not intend to create a DeFi ecosystem by reallocating revenue.

As of June 30, 2024, Tether Limited reported holding $118.4 billion in reserves, exceeding $113.1 billion in liabilities for Tether tokens by $5.3 billion, and earning a $5.2 billion profit for the first half of 2024.

This profit is mainly earned by interest-bearing U.S. Treasury Securities. It doubles the revenue of major blockchains, but Tether does not allocate a portion of its profits to USDT holders during periods of high interest rates to stimulate transaction activities. Conversely, users face risks related to Tether's potential bankruptcy and operational challenges.

The market demands yield-bearing stablecoins. To achieve this, decentralized stablecoins must have sustainable "Seigniorage" revenue sources and be allocated organically to DeFi activities in the ecosystem.

In this article, we will research the protocol architectures of Maker, Ondo, and Ethena alongside their respective stablecoins: Dai, USDY, and USDe.

Maker: Endgame

Protocol Information

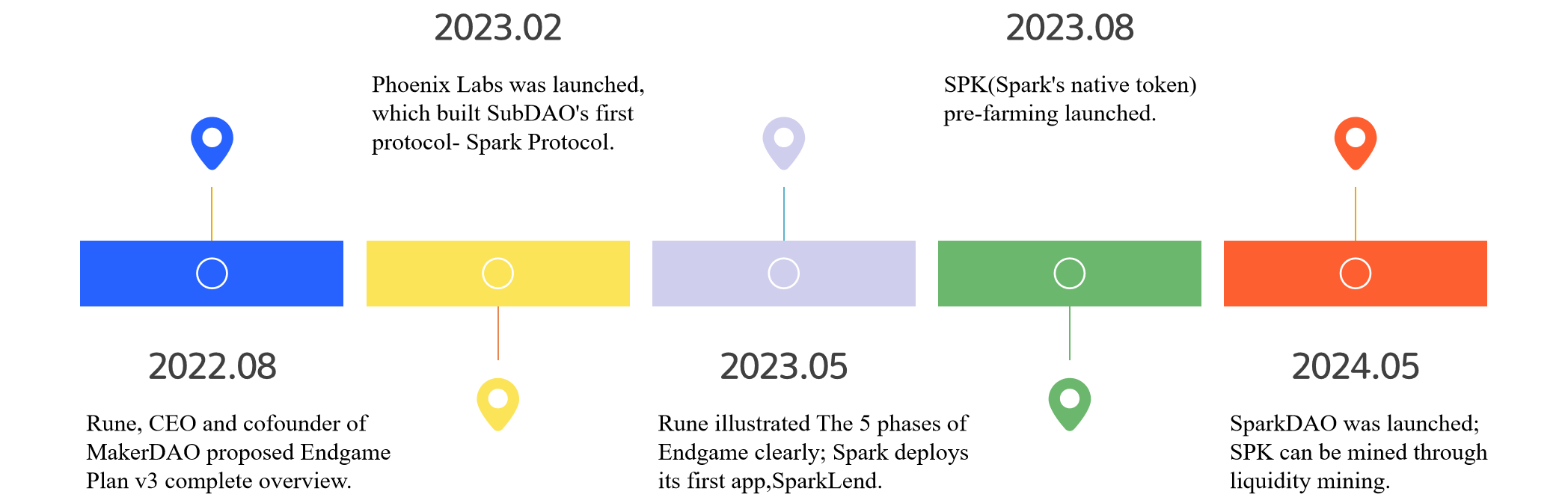

Maker is a protocol built on the Ethereum blockchain, aimed at providing a decentralized, over-collateralized stablecoin, Dai. MakerDAO, an open-source project established in 2014 on the Ethereum blockchain, oversees Maker's operation. As part of the Endgame plan, Maker is Reorganizing MakerDAO into SubDAOs with new tokenomics, and incorporating RWA to enhance the stability and yield of Dai.

Here is the progress of Endgame. Detailed information is provided later in the text.

Protocol Architecture

Dai is the biggest decentralized stablecoin with an over-collateralization mechanism in the Ethereum blockchain and Layer2s. To facilitate lending and borrowing, Maker has created a smart contract called a Collateralized Debt Position (CDP), which accepts pledged collateral tokens (such as ETH, wstETH, rETH, WBTC) and makes a Dai credit facility available. Dai is not subject to counterparty risks or traditional banking risks.

Borrowers borrow Dai by depositing collateral assets into Maker Vaults within the Maker Protocol. The initial Loan-to-Value ratio (LTV), which represents the ratio of a Dai loan to the value of its collateral, is determined by users and is between 0 and the Liquidation Ratio. In the process of borrowing, any Maker Vault whose current LTV exceeds the Liquidation Ratio must be liquidated through automated Maker Protocol auctions. To retrieve their collateral, borrowers have to repay Dai loan and the Stability Fee.

Dai holders(Lenders) deposit Dai to earn additional Dai from DSR (Dai Saving Rate, funded out of the Stability Fees paid by CDPs. For example, the average Stability Fees collected on CDPs is 8% to fund a DSR of 7%).

Tokenomics

There are two tokens in the Maker ecosystem now: Dai and MKR. Dai is a decentralized, over-collateralized stablecoin. MKR is the token with the utilities of Fees Payment, Governance Rights, Value Accrual, and Airdrop Credentials.

Dai

Market Cap: $5.35 billion (until 7/31/2024)

Volume(24 h): $124.95 million (Average volume between 7/29/2024 and 8/4/2024)

Holders use DAI mainly because of its pioneer advantage and network effects. DAI is adopted by many leading DeFi protocols and exchanges, and is included in the 3pool, the oldest stablecoin liquidity basepool.

MKR

Market Cap: $2.57 billion

FDV: $2.78 billion

(Data is collected until 7/31/2024)

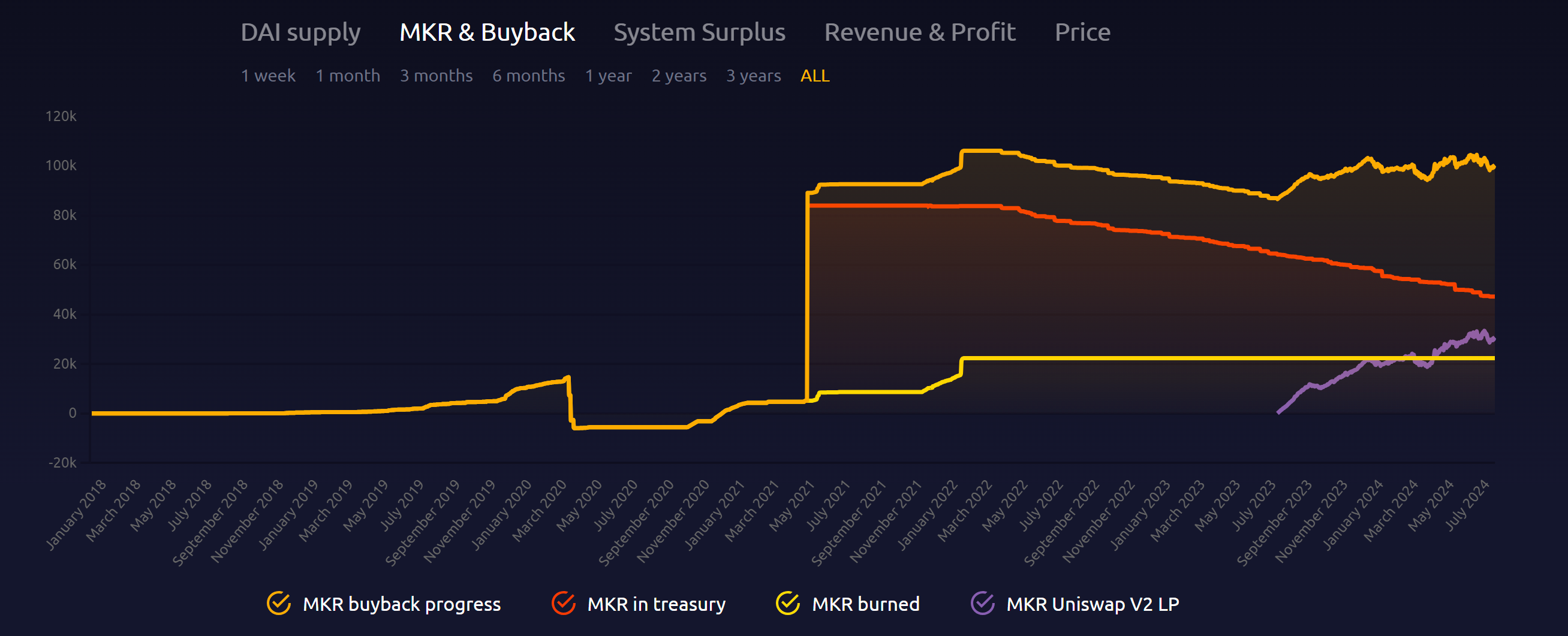

Now, all MKR are unlocked. MakerDAO has buy-backed about 100,000 MKR (10% of MKR's initial supply, which is burned in Uniswap V2 LP or treasury).

MKR is the token with utilities of Fees Payment, Governance Rights, Value Accrual, and Airdrop Credentials.

-

Fees Payment: MKR is required to pay the fees accrued on CDPs used to generate Dai.

-

Governance rights: MKR holders can vote on the Maker system's risk management and business logic, including the Stability Fee, Liquidation Ratio, and other key risk parameters. They can also vote on proposals to change the Maker Protocol, such as whether to turn to Endgame.

-

Value Accrual: If Dai proceeds exceed the Maker Buffer limit, overflow Dai is sold to buyback MKR, thereby reducing the circulating supply of MKR and increasing MKR's intrinsic value.

-

Airdrop Credentials: After the Endgame launch, NewGovToken is obtained by upgrading MKR at 1:24,000. Holders of MKR and NewGovToken can earn part of the Token Rewards from all other SubDAOs.

Endgame

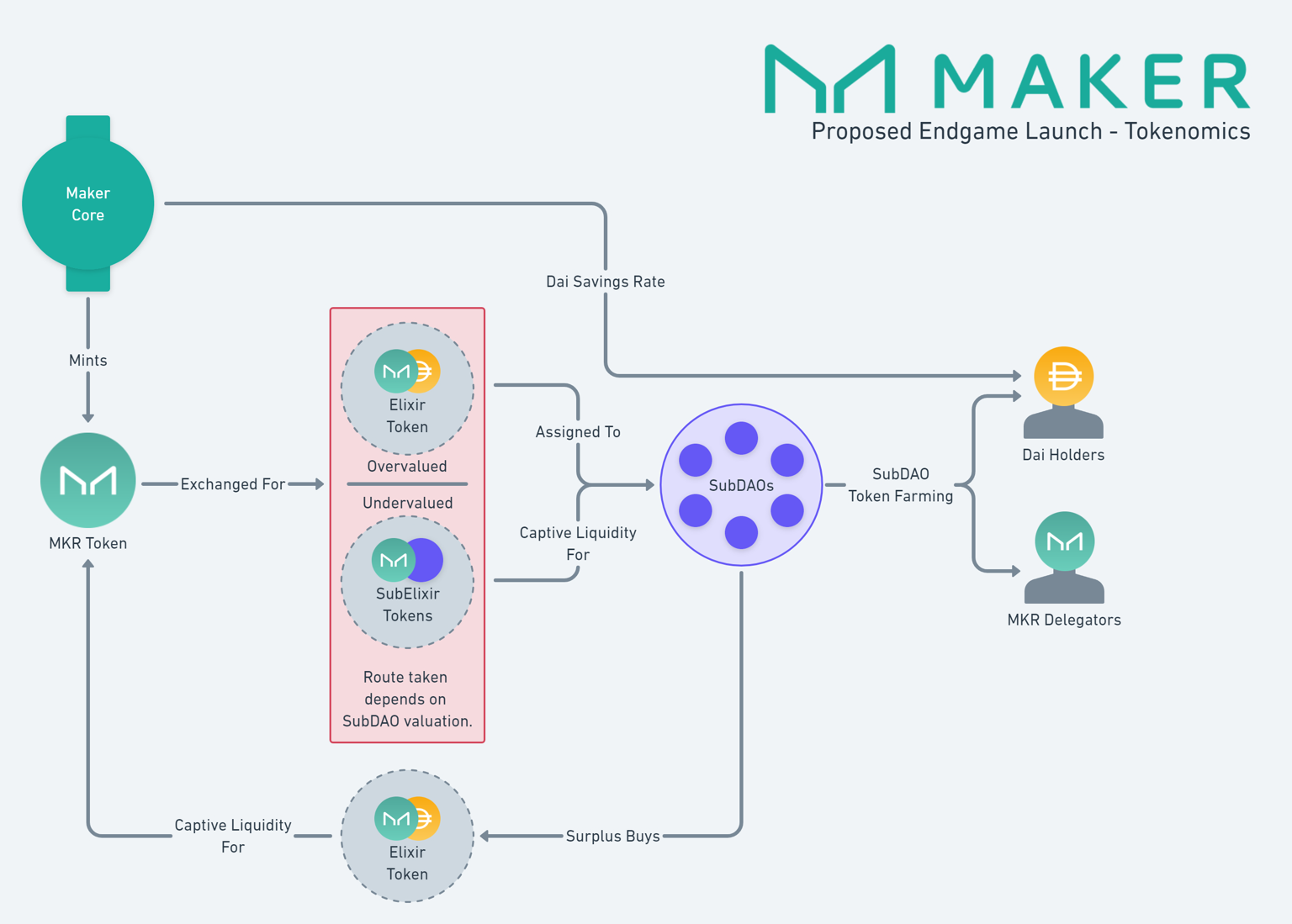

To address the issues of insufficient incentives in the Maker ecosystem, the lack of appeal due to low DSR, and the limited use cases for Dai, Rune proposed the Endgame Plan. The core of the Endgame Plan comprises two key elements: Reorganizing MakerDAO into SubDAOs with new tokenomics, and incorporating RWA to enhance the stability and yield of Dai.

Organizational Structure: New SubDAOs with new tokenomics

MakerDAO reorganizes the existing ecosystem into new, self-sustainable SubDAOs. Each SubDAO will have its unique governance token, NewGovToken(NGT), stablecoin, NewStable, governance processes, workforce, and interfaces.

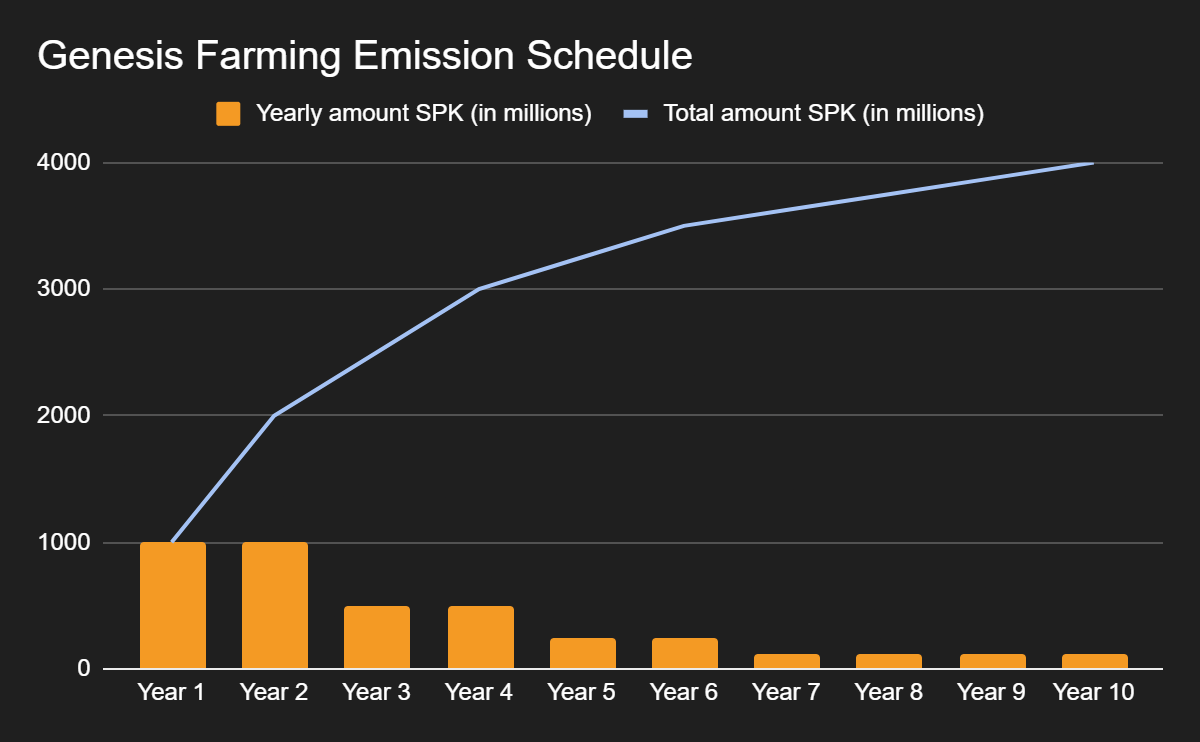

New tokenomics are created to reconcile relationships between Maker Core and SubDAOs by aligning incentive structures. The Dai and MKR tokens will remain, and conversion at fixed rates between them and new tokens is free. Maker Core emits a fixed amount of MKR annually to maintain sustainable liquidity for both MKR and Dai/Newstable while also supporting the development of SubDAOs.

Investors can lock up their MKR and NGT in Sealed Activation, enabling continued participation in governance. These locked-up MKR and NGT are eligible for farming rewards in Dai and SubDAO tokens. This mechanism is akin to the relationship between BNB, FDUSD, and new tokens in Binance's LaunchPool. MKR is poised to be the "Golden Shovel" in the Maker Ecosystem, Dai expands the use case of Yield Farming, and projects easily raise funds and achieve cold starts.

In Endgame, it's also planned to build the NewBridge system for inter-blockchain bridging, introduce AI tools to assist governance and create a stand-alone L1 NewChain to host the core tokenomics and governance mechanics of Maker Core and the SubDAOs, finally achieving a dynamic, ever-growing ecosystem.

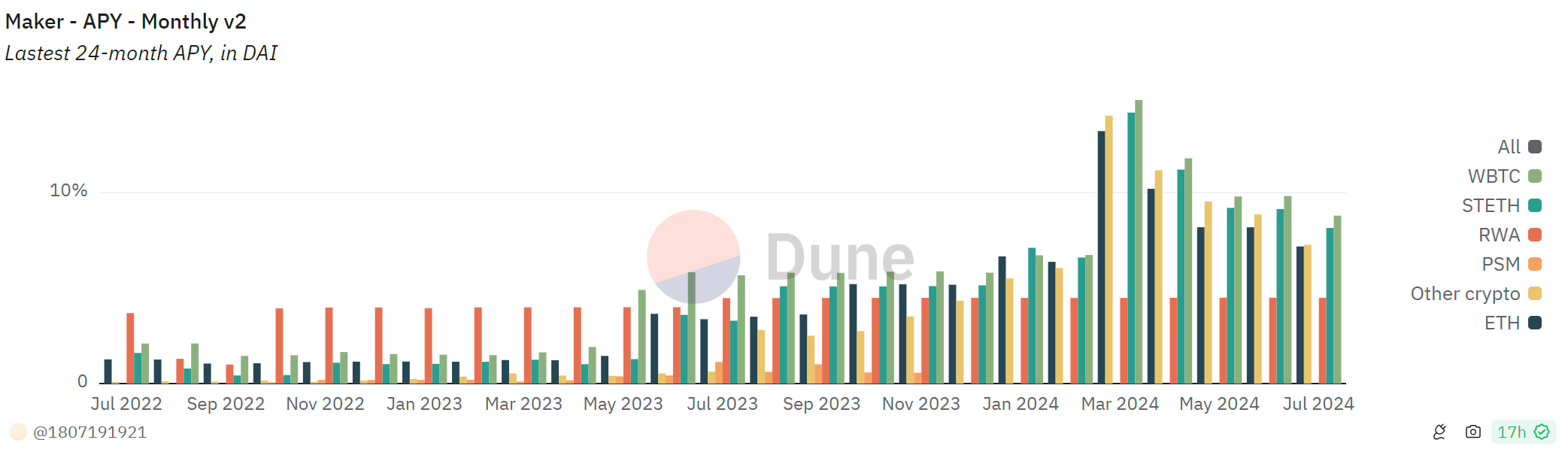

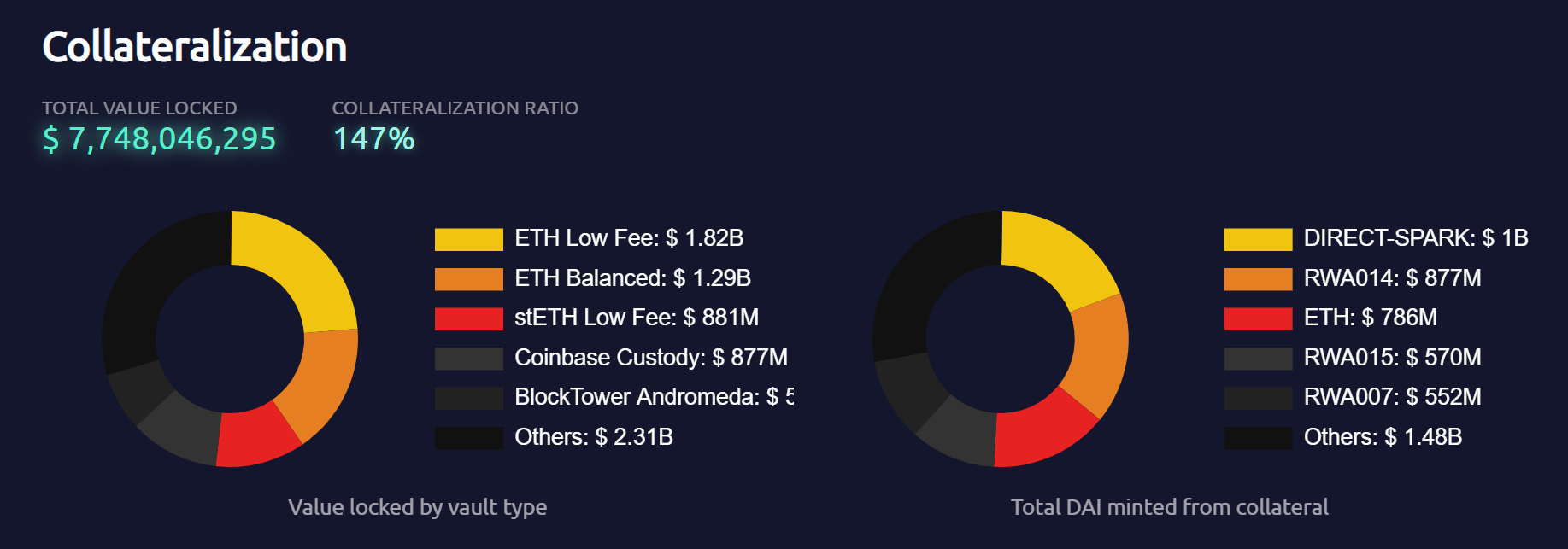

Assets Structure Introduction of RWA

In Endgame, the Introduction of RWA brought over $2 billion in collateral with about 4% APY, helped maintain the total collateral scale at $5 billion, and turned negative earnings between Q3 2021 and Q2 2022 into positive earnings. If RWA retains the scale of 2024's first half, RWA's profit in 2024 can reach $80 million.

RWA's proportion in total Dai minted from collateral increased to about 40%. By shifting collateral from non-interest-bearing stablecoins (USDC, GUSD) to treasury bonds or stablecoin financial products, MakerDAO has markedly improved its anticipated revenue, reflected in a decrease in the PE ratio from 100× to 30×. But this shift is unsustainable:

-

First, there is still $500 million in stablecoin collateral, accounting for just 6.5% of the total collateral. The purchasing power of the remaining reserve is not enough.

-

Second, the SEC easily prosecutes the continuing introduction of treasury bonds. Concentrating heavily on treasury bonds weakens Maker's decentralization and censorship resistance.

-

Third, the Effective Federal Funds Rate (EFFR) has maintained a high level of 5.33% for one year. The Fed has turned dovish, and the forecasted earliest rate cut is in September 2024. RWA's high APY is likely to decrease to less than 3%.

Spark

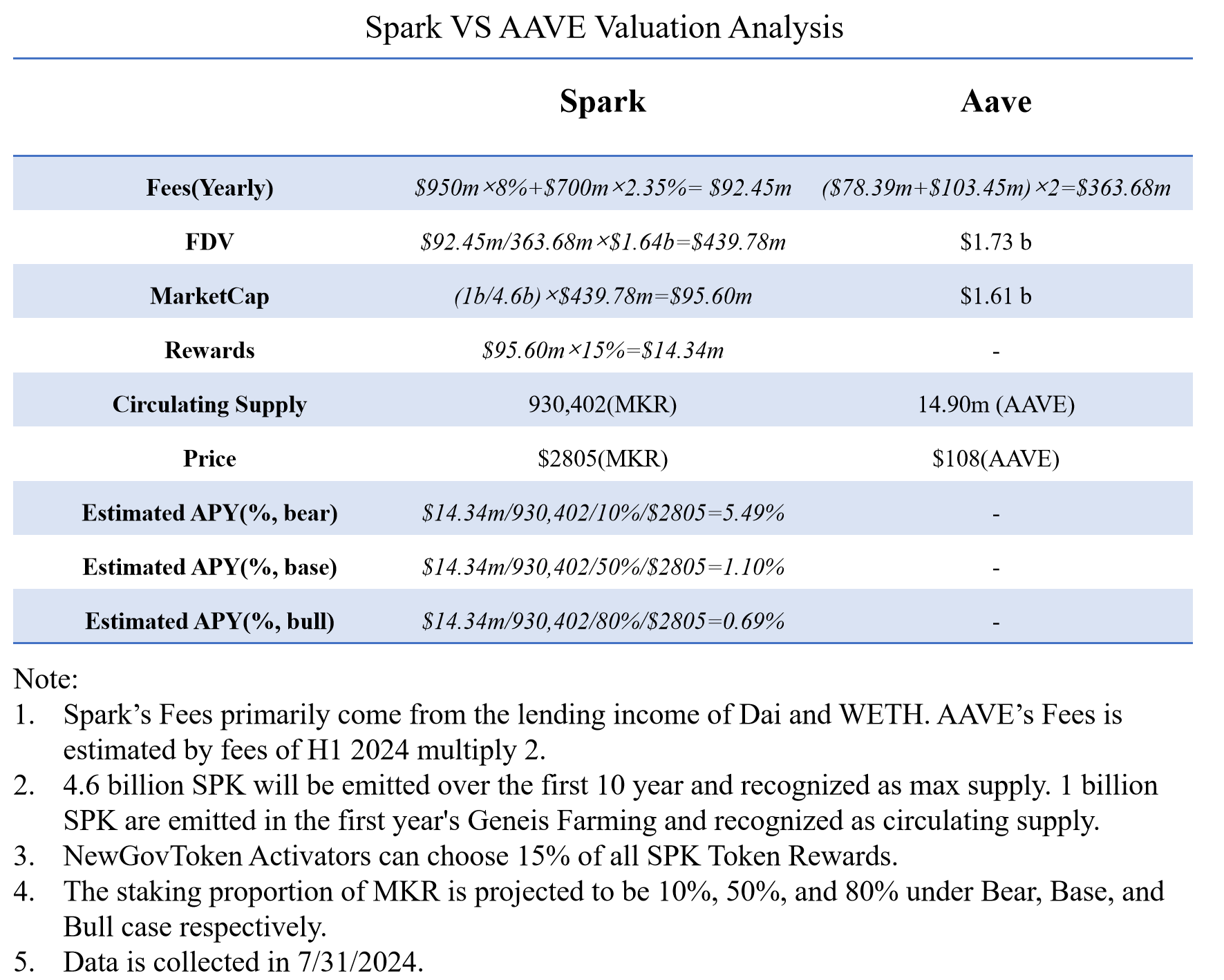

Spark is Maker's first SubDAO, a DeFi lending platform. It's a fork of Aave's v3, allowing users to interact with DAI through borrowing, lending, and staking. To boost the cold start, users of SparkLend can farm the Spark airdrop, which will grant them SPK tokens when Spark fully launches.

Spark has a TVL of approximately $3.2 billion, making it the third-largest lending protocol. The supply liquidity amounts to $4.9 billion, but the utilization rate is only 35%, which means the protocol surplus is close to 0.

NewGovToken Activators can choose 15% of all SPK Token Rewards. Hence, by using the P/F ratio—defined as fully diluted market cap divided by annualized fees—and taking AAVE as a reference, we can estimate Spark's fees, valuation, and potential price increase of MKR.

According to estimates, when the MKR staking proportion is below 36%, the expected yield for MKR will exceed 2%.

Ondo: Compliant RWA

Ondo Finance is an RWA tokenization investment protocol that democratizes institutional-level investment opportunities. Ondo introduces low-risk, stable, interest-bearing, scalable fund products, such as U.S. Treasury bonds and money market funds, to the blockchain. This provides on-chain investors a viable alternative to stablecoins, allowing asset holders to capture the most returns from the underlying assets rather than the issuers.

Ondo Finance was founded by former Goldman Sachs employees Allman and Pinku Surana. Leveraging their extensive network, Ondo raised $34 million from Pantera Capital, Bixin Ventures, and other prominent VCs.

The Ondo USDY LLC-issued USDY is a tokenized note that combines the stability of a conventional stablecoin with the yield potential of high-quality US dollar-denominated assets. USDY is designed for non-US individual and institutional investors seeking an alternative to conventional stablecoins with the added benefit of earning yields from the underlying assets.

Here are the highlights of USDY.

-

Yield generation is USDY's distinguishing attractiveness. While stablecoin holders (USDT, USDC) typically do not receive direct interest in their holdings, USDY holders enjoy the yield generated from the underlying short-term US Treasuries and bank demand deposits. This offers a potentially attractive return on investment. Now, USDY's APY is up to 5.3%.

-

Regulatory compliance is the cornerstone of USDY. Issued in accordance with US federal and state securities laws and financial crime compliance regulations, USDY avoids the regulatory gray area often associated with stablecoins. For example, investors must complete the KYC process, sign the appropriate paperwork, and redeem USD via bank wire to non-US bank accounts.

-

A special organization structure and third-party verification secure USDY. It is issued by Ondo USDY LLC, a company designed to be bankruptcy-remote from any other entities, including Ondo operating companies. (Even during Ondo's bankruptcy, USDY holders won't lose their USDY.) Ankura Trust Company protects USDY holders as a Verification Agent and Collateral Agent.

-

Continuing collaborations with TradFi, CeFi, and DeFi expand USDY's applications. USDY is accessible to the 90+ chains in the Cosmos ecosystem through Noble. USDY also launched on Ethereum and its Layer2, Solona, Injective, Aptos, Sui, and other blockchains; Arbitrum DAO Votes to Allocate 17% of Treasury Diversification to USDY. Good collaboration is still continuing.

In summary, USDY offers a novel approach to stablecoin investment, providing the security of a US government bond-pegged asset with the added benefit of yield generation. Its robust legal framework, asset-backed structure, and transparent yield distribution make it an innovative choice for institutional investors, especially those suffering rampant inflation of developing countries' native currencies, looking to diversify their portfolio with a stable and potentially rewarding asset.

Ethena: Crypto Market Native Yield

Protocol Information

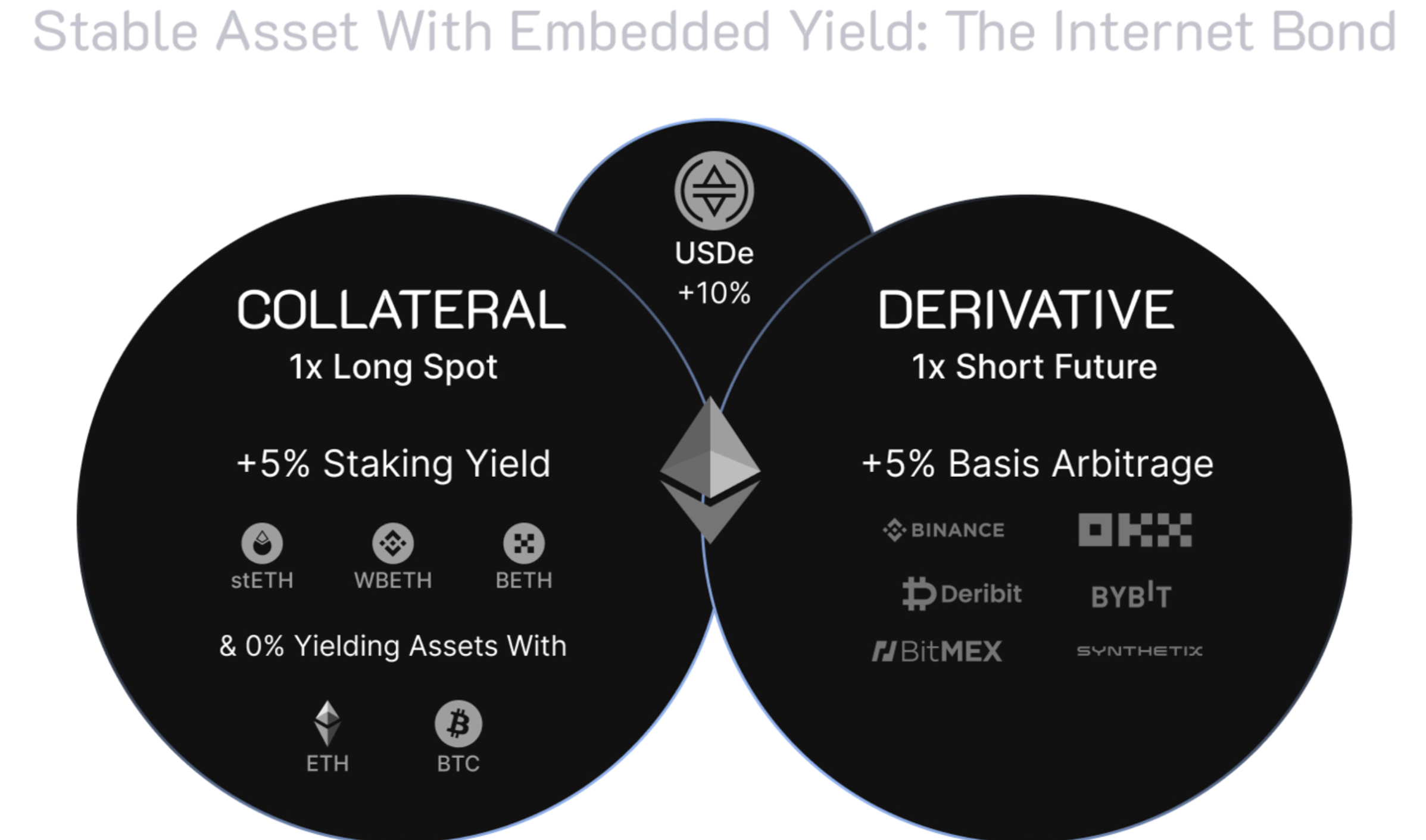

Ethena is a synthetic dollar protocol built on Ethereum. Its synthetic dollar, USDe, offers a crypto-native, scalable and reward-bearing stablecoin solution through delta-hedging of Ethereum and Bitcoin collateral. Ethena was inspired by Arthur Hayes' 2023 blog post "Dust on Crust". As the founder of BitMEX and the family office Maelstrom, Hayes has significantly accelerated Ethena's development. In 2023, Maelstrom supported Ethena's $6.5 million seed round, with Hayes also serving as the founding advisor of the project.

Protocol Architecture

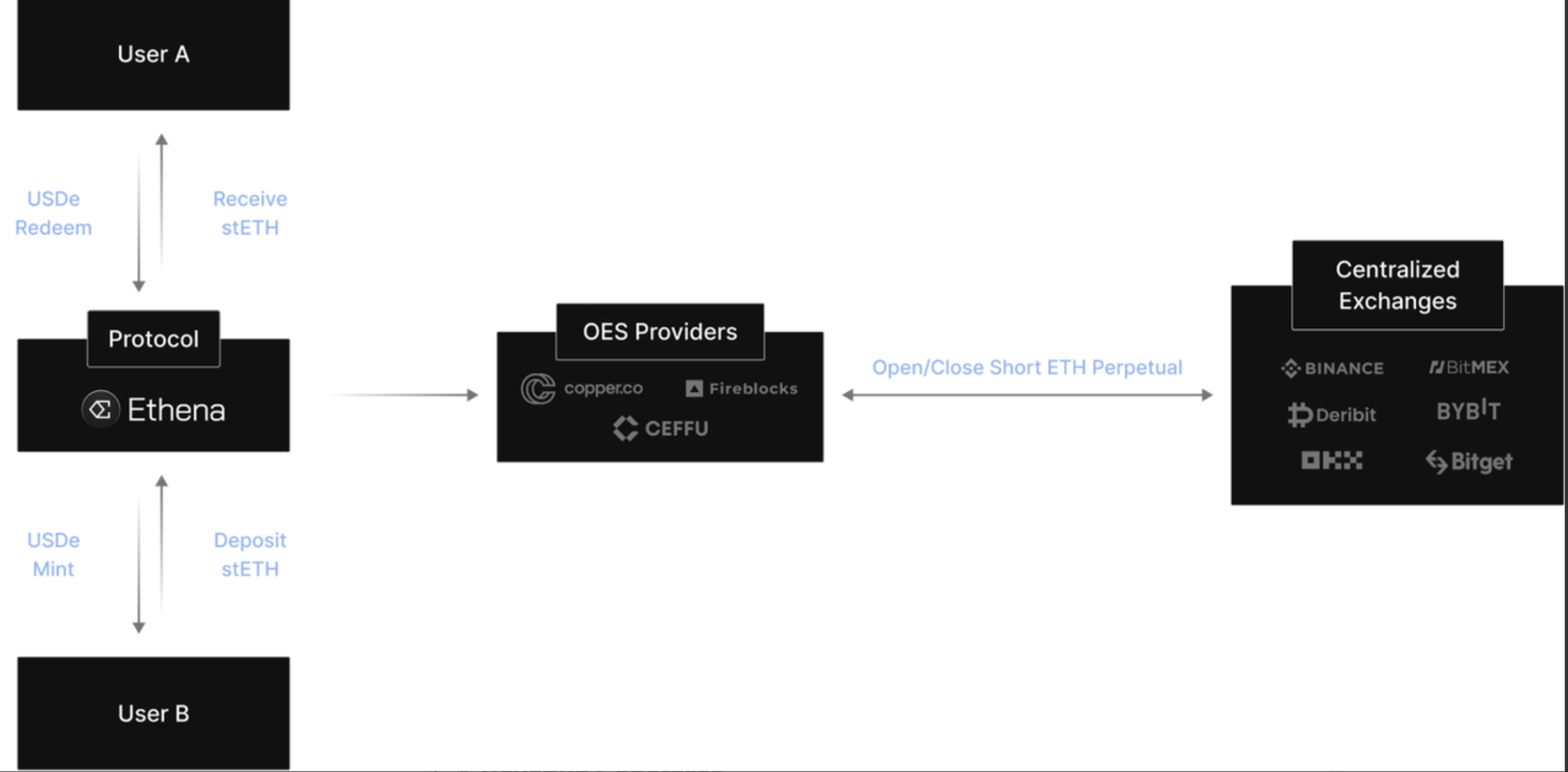

Ethena utilizes a delta-neutral strategy to support the stability of synthetic dollar USDe. The Ethena protocol deposits backing assets (such as stETH and BTC) provided by whitelisted users directly to an "Off Exchange Settlement" solution and, at the same time, opens a corresponding short perpetual position for the approximate same notional dollar value on a derivatives exchange. The delta-neutral strategy ensures the portfolio value in USDe is unchanged despite changes in the value of the underlying collateral.

Revenue Generator

The Ethena protocol generates two sustainable sources of yield from the backing assets.

Protocol Revenue = Staked ETH rewards + The funding and basis spread.

Staked ETH assets receive consensus and execution layer rewards

Since the transition to PoS, holding liquid staking Ethereum tokens has generated a variable yield, which is about 3%-4% now.

However, Bitcoin and other non-stakable assets cannot produce staking revenue. As a result, when the proportion of Bitcoin holdings increases to around 50%, the overall staking annual percentage yield (APY) is reduced to approximately 1.5%-2%. Despite this, the staking revenue from ETH continues to offer a positive margin of safety for the protocol's revenue.

The funding and basis spread from the delta hedging derivatives positions

Given the mismatch in demand and supply for crypto, the funding and basis spread have historically generated a positive yield. Therefore, Ethena's long positions of spots and short positions of perpetual contracts construct a profitable arbitrage portfolio. The funding and basis spread contribute to the main revenue source of the protocol.

However, in bear markets or market crashes, the funding and basis spread can turn negative, reducing protocol revenue below staking revenue. In such cases, Ethena's reserve fund will bear associated costs.

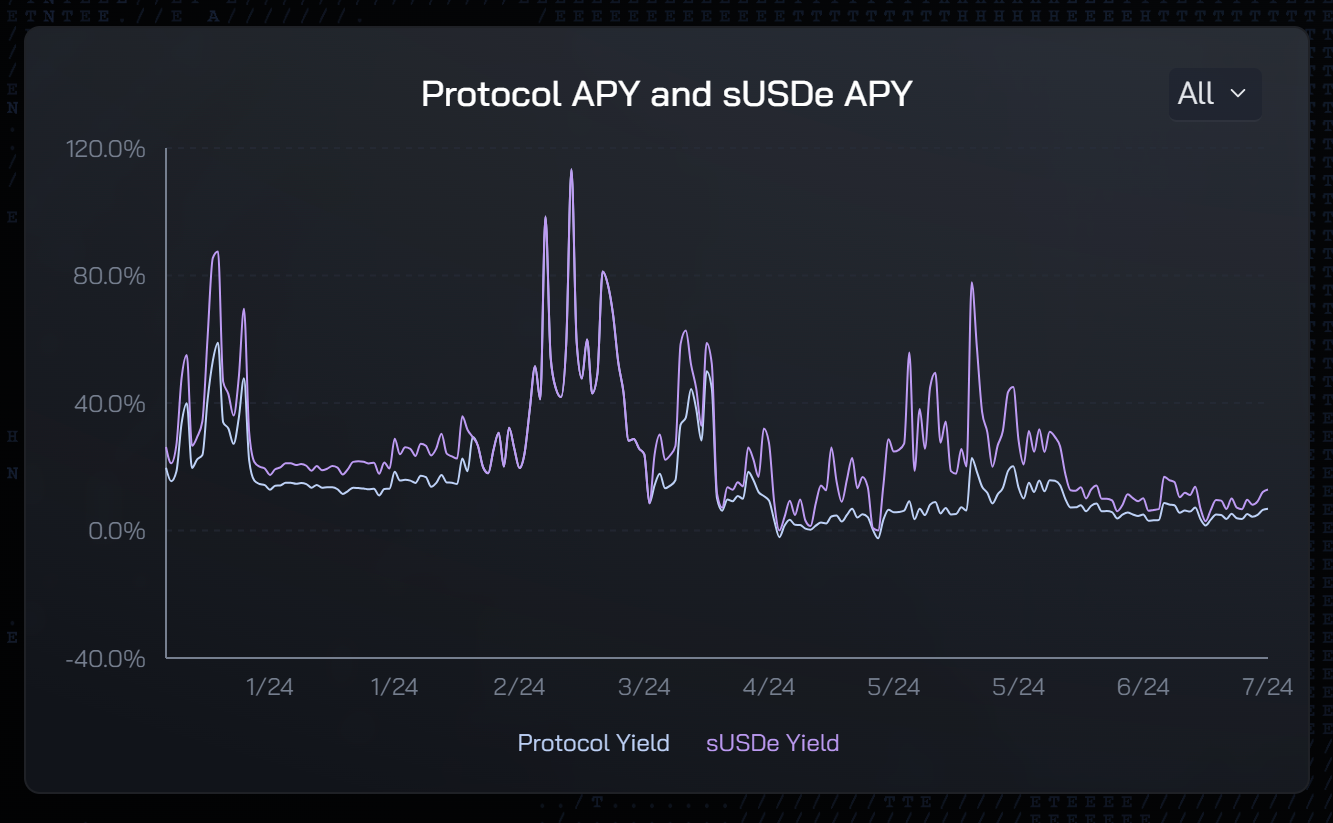

Until July 2024, the market cap of USDe was about $3.2 billion, and the scale of the reserve fund reached $46.5 million. It means only when APY of the funding and basis spread reach -3%, reserve fund will be depleted in a year. However, despite history's bear market and market crash, the USDe yield is still positive. The security of reserve funds is high.

The scale of USDe's Reserve fund and USDe's liquid cash is about $300 million until 7/24/2024. There is a lot of potential to allocate idle capital. Allocation to BlackRock's BUIDL, expands a new revenue source from RWA, and diversified investments help hedge against low funding returns and basis spread.

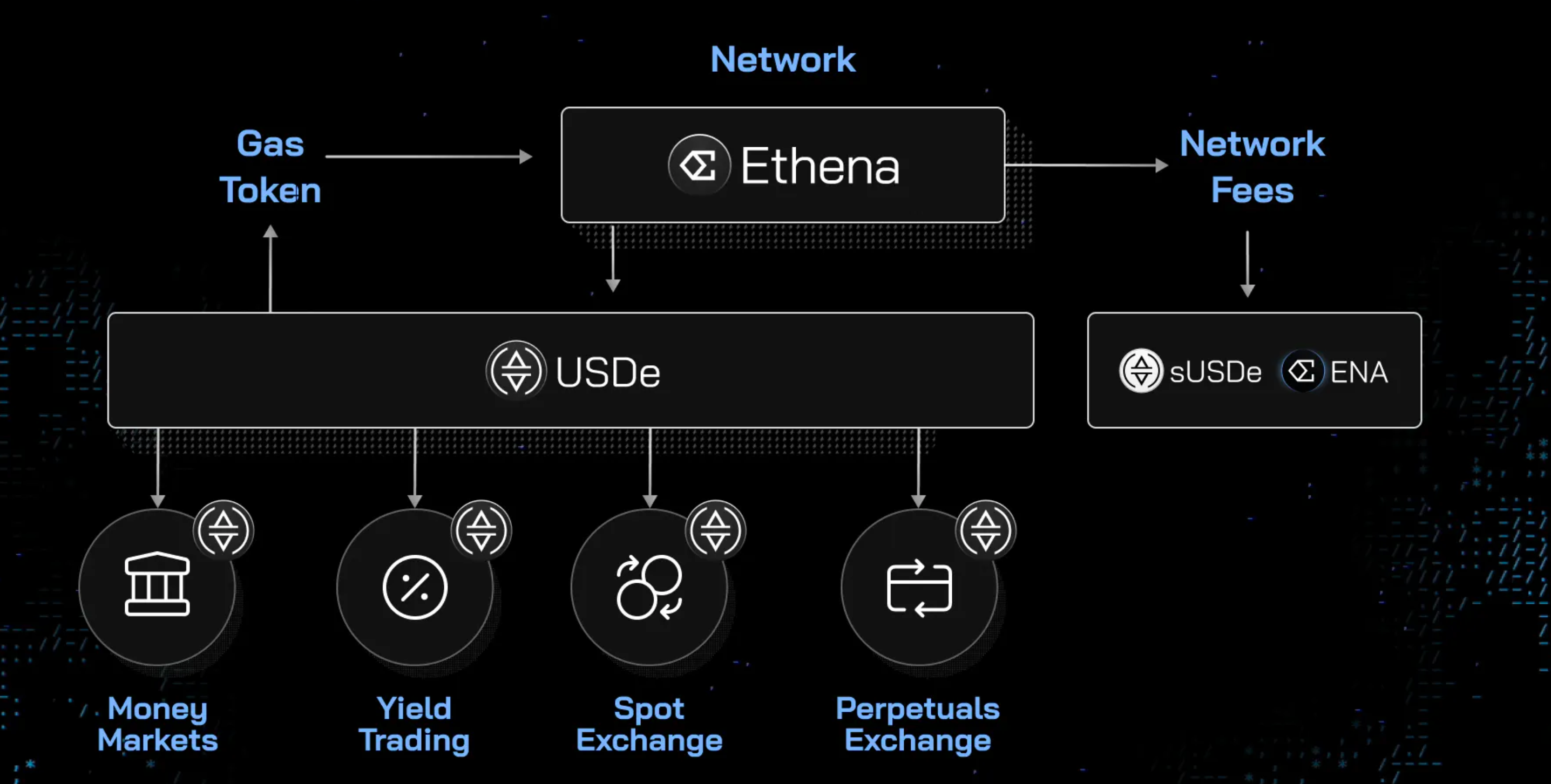

Tokenomics

The Ethena ecosystem has three tokens: USDe, sUSDe, and ENA. USDe is the stablecoin of the Ethena ecosystem. sUSDe is the staked form of USDe, which captures Ethena's protocol revenue. ENA is the governance token of Ethena.

USDe

Market Cap: $3.2 billion (On 7/31/2024)

Volume(Daily average volume): $91.4 million

sUSDe: $1.5 billion (On 7/31/2024)

ENA

Market Cap: $705 million (On 7/31/2024)

FDV: $6.2 billion (On 7/31/2024)

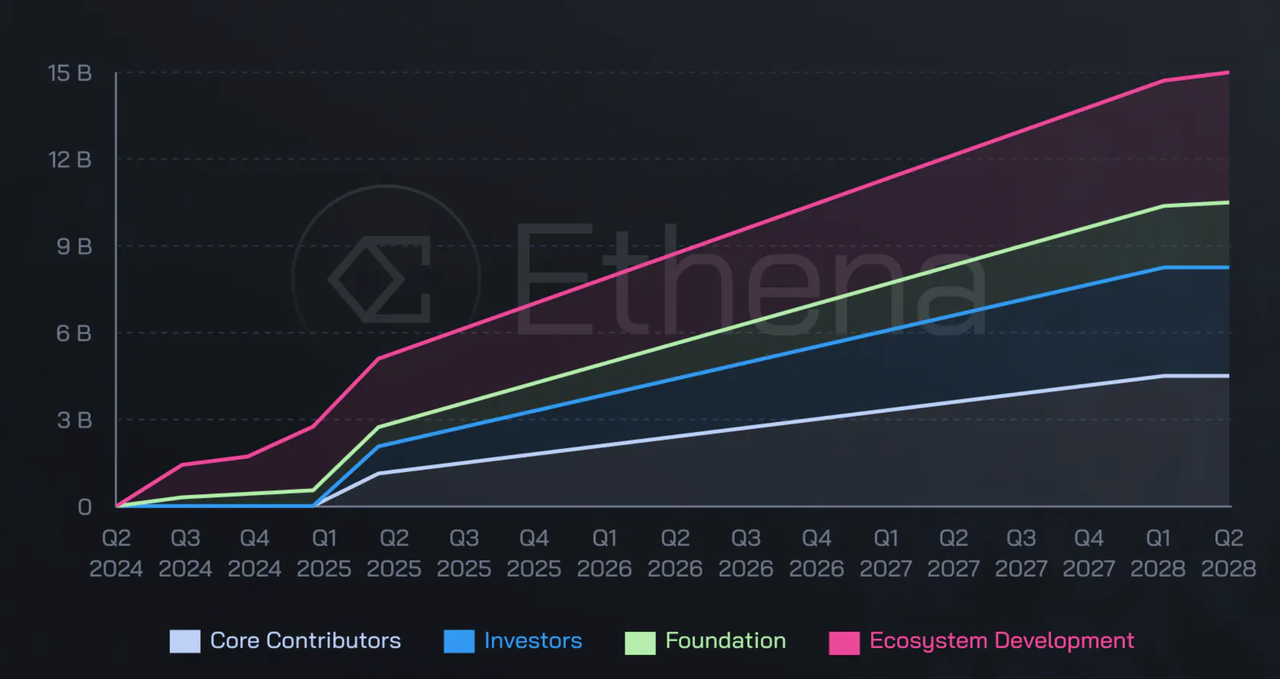

Distribution and Vesting Schedule:

The Market Cap/FDV is just 11.38% up to July 2024. After Q1 2025, the scale of linear vesting is great until Q1 2028, which will cause continual and heavy selling pressure for the price of $ENA. By August 1, 2025, the Circulating Supply of $ENA will reach 5.36 billion. The expected inflation rate will be 213% in the following year.

Roadmap Update

USDe

Ethna's goal is to construct a Unified Money Layer based on USDe. The most important thing for USDe is to expand the range of its applications: USDe can directly value more assets and settle more transactions and activities. In Ethena's statement, USDe can be used to pay future Gas Token and network fees.

USDe's mint mechanism contributes to CEXs' deep liquidity, making collaboration between Ethena and CEXs easy to expand. Ethena has collaborated with Bitbit and Bitget, and USDe will settle more transactions. USDe has already been added as

reward-bearing stable margin collateral in Bybit.

However, the total perpetual futures OI is the noticeable ceiling for USDe's growth because every USDe's mint corresponds to equal amounts of short positions. According to the Ethena website, the BTC Open Interest is 23.23B, and ETH Open Interest is 11.31 B. Ethena would have to increase its OI proportion to 50% to be capable of issuing $20 billion USDe.

At the same time, massive Ethena's OI will exert significant downward pressure on the market; the funding rate will decrease, reducing USDe's attractiveness.

In addition, high APY is the main reason users use USDe other than USDT. Despite this, Ethena's business moat is not particularly wide. Currently, Ethena functions more like a large quantitative arbitrage fund. Many other quantitative funds achieve an average APY of over 20% and offer greater flexibility by transacting in a wider range of cryptocurrencies with higher APYs. If USDe attracts investors solely based on APY, some may prefer to invest in these specialized quantitative arbitrage funds.

For USDe, the negative correlation between the size of the issuance and the rate of return is deeply rooted in its Protocol Architecture. This indicates that its revenue is from the crypto market rather than the extrinsic traditional US Dollar market. Hence, the APY of USDe can be considered the risk-free rate of the crypto market and a popular financial product for yield trading in IRS platforms such as Pendle. In the future, every investment less than USDe's APY will be considered less attractive. The wide application of USDe will set a new benchmark rate for the whole crypto market.

ENA

ENA is Ethena's Governance token. Holders can vote on governance proposals regarding the Ethena protocol, such as general risk management frameworks, USDe backing assets composition, Distribution allocation between sUSDe and Reserve Fund, etc.

The next phase of incorporating ENA into the Ethena system and adding utility will leverage generalized restaking pools for staked $ENA. As detailed in the 2024 roadmap, the Ethena Chain will be focused on building financial applications and infrastructure for $USDe as the gas token and fulcrum asset within the system. New utilities help construct intrinsic values of ENA:

-

Gas Fees paid by USDe: Users pay gas fees by USDe, and USDe will be rewarded to ENA stakes for providing generalized security across each use case.

-

Airdrop expectations: Well-developed projects in the Ethena ecosystem are likely to airdrop to ENA holders.

The first use case is to provide economic security for cross-chain transfers of USDe relying on the LayerZero DVN-based messaging system by utilizing the Symbiotic restacking framework. This is the first of multiple layers of infrastructure related to the upcoming Ethena Chain and financial applications built upon the chain, which will utilize and benefit from restated ENA modules.

Ethena's TVL is now $3.1 billion, ranking eighth among all DeFi protocols. Construction of Ethena's ecosystem is still early.

Conclusion

Key similarities among these stablecoins include:

-

Expanding Use Cases and Extending to Multi-chains: The sum of DAI, USDY, and USDe's daily volume is less than 0.5% of USDT. Stablecoins need diverse use cases to broaden application scenarios and maintain decentralization. Collaborating with mainstream CEXs and DEXs, partnering with financial institutions, and using DeFi protocols are critical for mass adoption. Extending to multiple blockchains is also essential, and autonomous Chain is the destination.

-

Introduction of RWA: Integrating RWA is a common strategy among stablecoins during high interest rates. However, attractive yields may not be sustainable when rates are cut.

-

Significance of Interest Rates: Stablecoin interest rates are crucial and can be regarded as DeFi benchmarks. Relevant Interest Rate Swap (IRS) products, such as those offered by Pendle, can help stabilize the position of the corresponding stablecoin.

A distinct investment thesis supports each project discussed in this article:

Interest in USDe and ENA increases when the market is in the bull cycle, and the funding rate is high because investors mainly focus on USDe's high APY.ENA could be a good buy during the “low funding rate” period in the bull cycle and a good exit during the “high funding rate” period, and locking $ENA within Pendle Finance PT-ENA and going short ENA perpetual contracts is a clear arbitrage chance. Be cautious about adding to position between Q1 2025 and Q2 2025 lest huge amounts of unlocking.

Ethena's business moat is not particularly wide, and currently, Ethena functions more like a large quantitative arbitrage fund. For example,

Elixir launched a homogeneous deUSD with $1 billion in liquidity lined up to challenge Ethena's USDe.

Interest in MKR and Dai increases when Endgame proceeds smoothly. MKR could be a good buy when airdrops of SubDAOs are launched and a good exit when no more airdrops or the relationship between MakerDAO and SubDAOs is confused.

Interest in Ondo increases when traditional financial institutions buy tokenization RWAs.Ondo could be a good buy when collaborating with financial institutions from Wall Street or government departments and a good exit when the scale of RWWs stagnates, but EFFR begins to decrease.