English

Request a demoMarket Updates

The DeFi Bedrock: Money Market Protocols

20 Mar 2025

Introduction

Market sentiment has significantly cooled following the retracement of Bitcoin’s price from its $100K peak, the fading AI agent frenzy, and the collapse of the LIBRA rug pull further highlighted the extent of insider manipulation against retail participants in memecoin trading. Amid widespread panic selling and speculation about the cycle top, investor focus is shifting back to DeFi protocols that generate real revenue, as opposed to speculative assets like memecoins. Notably, DeFi mindshare tracked by Kaito has increased from 4.5% to 15%. Within the DeFi space, lending protocols have shown particularly strong and resilient growth, even in the face of early 2025’s bearish market conditions. In this article, we’ll explore the competitive advantages, or moats, of today’s leading blue-chip lending protocols and rising stars, and provide a comparative analysis of their key metrics.

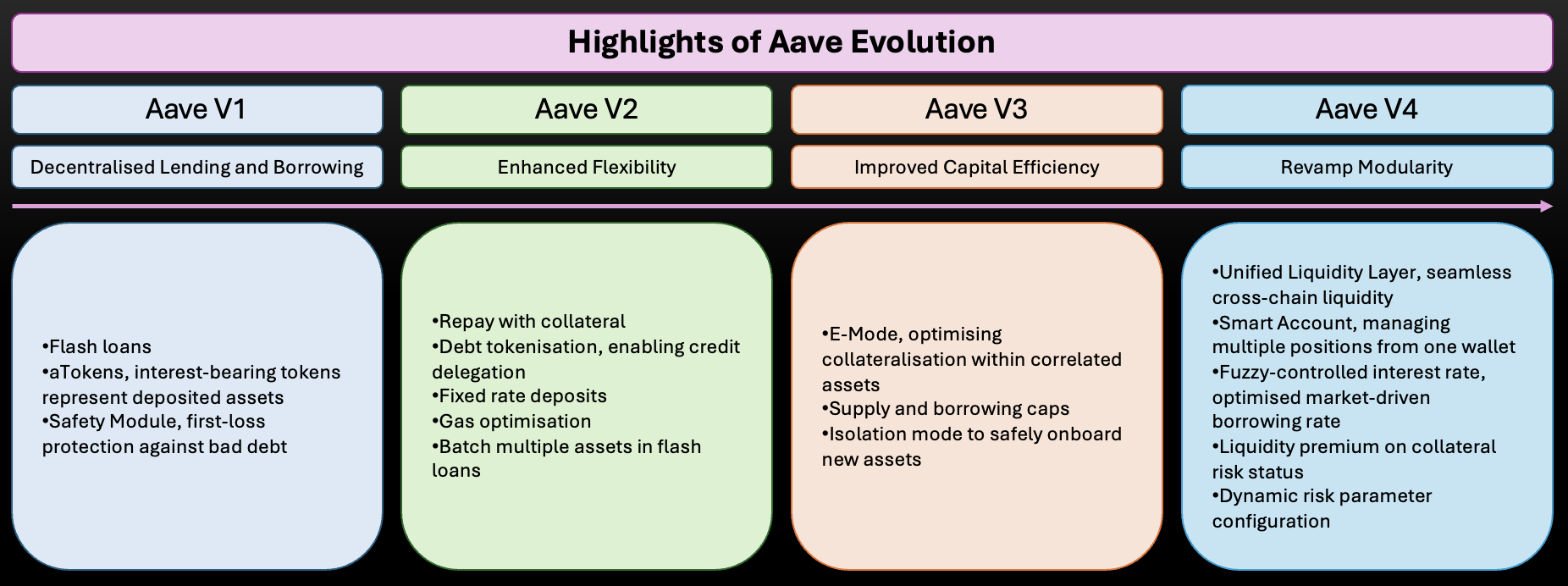

The King of Lending Protocols: Aave

Aave continues to dominate the lending sector, consistently leading in Total Value Locked (TVL), outstanding loans, and revenue generation. As the juggernaut of lending protocols within EVM-compatible networks, Aave has expanded beyond its Ethereum roots to Aptos, marking its first deployment on a non-EVM chain.

Alongside Aave V4, stakeholders should anticipate the Umbrella Upgrade, a significant enhancement to the Aave Safety Module (ASM). Key features include:

-

Allowing users to use aTokens as collateral within the ASM

-

Introducing automatic asset seizures and per-network collateral management

-

Improved incentive mechanisms with potential additional yield via slashing hooks

-

Expanding stkAAVE coverage to DAO-approved external markets

Additionally, AAVEnomics is set to launch soon. As part of its new financial framework, the protocol will implement a weekly $1 million AAVE buyback program for an initial period of six months. This initiative will be overseen by newly established Financial Committees to ensure transparency and accountability.

A growing number of protocols are adopting licensed instances of Aave’s technology, particularly Aave V3 and the forthcoming V4. Notable examples include:

-

World Liberty Finance, which runs an Aave V3 instance and returns 20% of its protocol revenue to Aave, alongside allocating 7% of its token supply to the Aave ecosystem.

-

Horizon Protocol, an upcoming initiative focusing on real-world assets (RWA) and institutional adoption, plans to use licensed Aave V3 and V4 instances upon release.

Additional protocols such as Spark, SuperLend, ZeroLend, RealT, and Reental have pledged to share a portion of their protocol revenues with Aave. However, decentralised governance remains a challenge. For example, disputes have arisen, such as the conflict between Aave and Spark over revenue-sharing agreements. Aave delegates accused Spark of employing “creative accounting” to reduce its revenue share payments from the agreed 10% to approximately 1%.

Pioneer of the Permissionless Lending Market: Morpho

Morpho Architecture

Morpho has taken a distinct approach to decentralised lending, diverging from the traditional DAO-governed model exemplified by Aave. Rather than relying on a centralised governance process to define risk parameters, Morpho empowers third parties to manage risk independently. The protocol enables anyone to create fully permissionless lending markets with customisable parameters including collateral and loan assets, liquidation loan-to-value ratios (LLTV), oracle selection, and interest rate models (IRM). Once a market is deployed, these parameters are immutable, secured by Morpho’s minimal 600-line smart contract codebase, ensuring trust-minimised and transparent lending environments. To simplify risk management for users across the diverse landscape of permissionless markets, Morpho offers Morpho Vaults, a curated strategy vaults that automatically allocate capital to specific lending markets. These vaults optimise returns while managing risk, making the protocol more accessible and efficient for both retail and institutional participants. Morpho’s permissionless model has gained substantial traction, attracting over $4.8 billion in total assets deposited.

Demonstrating its institutional potential, Coinbase leveraged Morpho’s infrastructure to launch Bitcoin-backed USDC loans, underscoring the protocol’s growing credibility and adoption. Additionally, Morpho-powered vaults have been integrated into established DeFi lending protocols, including Compound, Spark, Moonwell, and others, further solidifying its position in the DeFi lending space.

Morpho also licenses its technology to third-party ecosystems, such as Berachain, creating an additional revenue stream. Importantly, 100% of these licensing grants are allocated to supporting and enhancing the Morpho protocol, helping to offset development costs, operations, and frontend maintenance, while reducing reliance on MORPHO token emissions to fund the team. In line with its sustainability efforts, Morpho has recently reduced its token emissions by 25% as of February 2025, with plans to continue this gradual reduction over time. Currently, the protocol does not charge fees on lending markets, but it has a built-in fee switch mechanism. This functionality allows Morpho to enable fees ranging from 0% to 25% of the total interest paid by borrowers in any given market, providing a future pathway for protocol revenue generation.

Forkonomics and User-Set Interest Rates: Liquity

Liquity Forkonomics

The concept of Forkonomics, a term popularised by Liquity, offers a fresh perspective on the economic dynamics of protocol instances and forks. Liquity V1 was once a groundbreaking, immutable borrowing protocol for ETH-backed loans, peaking at over $4.5 billion in TVL during 2021. However, with the rise of competition, Liquity V1 was forked over 37 times, according to DefiLlama and the prolonged bear market of 2022 and 2023, Liquity’s market dominance gradually eroded.

Despite these challenges, the Liquity team made a strong return with Liquity V2, introducing a novel user-set interest rate model that has reignited market interest. This innovation gives borrowers the ability to select their own interest rates, fundamentally changing the dynamics of risk and capital efficiency within the protocol. In V2, Loans with lower interest rates are more susceptible to redemption risk, particularly during repegging events, and are subject to no haircut on redemption. Loans that exceed their loan-to-value (LTV) thresholds are exposed to liquidation risk, with penalties applied upon liquidation. The introduction of user-set interest rates is a significant advancement, as it empowers borrowers to optimise capital efficiency and maximise yields, particularly attractive for yield farming strategies.

Liquity V2 launched in collaboration with several leading networks, including Arbitrum, Base, Scroll, Berachain, HyperEVM, and others. The broader ecosystem has shown strong support; for example, Ironclad announced it would allocate 5% of its token supply to BOLD holders, the stablecoin introduced in Liquity V2. A standout feature of V2 is its value accrued model, designed to generate sustainable returns for participants:

-

25% of protocol revenue is directed towards third-party platforms like Curve and Uniswap, where it is used to bribe for gauge votes, incentivising liquidity.

-

75% of the revenue, along with liquidation gains, is distributed to the Stability Pool in BOLD. Stability Pool participants earn rewards by lending BOLD to liquidators, further incentivising protocol stability.

Unfortunately, Liquity V2’s Stability Pools, released in February 2025, encountered technical issues that affected their intended functionality. Given the immutable nature of the protocol, the team has opted to redeploy V2 in April 2025, addressing these issues in a new deployment while maintaining the integrity and trustless nature of the system.

Reborn and Reinvented Modularity: Euler Finance

Euler Finance TVL and Borrowed Amount

Security is paramount in the world of lending protocols, any vulnerability can result in catastrophic losses and irreparable damage to a protocol’s reputation. Euler learned this lesson the hard way. In March 2023, the protocol suffered a devastating flash loan exploit, resulting in the loss of $197 million in user funds. Although the Euler team successfully negotiated with the attacker to recover the majority of the stolen assets, the damage to its reputation was profound. For over a year, the protocol operated under a cloud of uncertainty. However, in September 2024, Euler made a remarkable comeback with the launch of Euler V2, a highly modular and permissionless lending framework. To restore user confidence, Euler V2 underwent 31 independent audits, demonstrating a rigorous commitment to security and resilience.

Euler V2 adopts a similar permissionless approach to Morpho, empowering anyone to create highly customisable lending markets via the Euler Vault Kit (EVK). Built on the ERC-4626 vault standard, this framework allows for the creation of both governed vaults, which include a designated risk manager and ungoverned vaults, giving users unparalleled flexibility in risk management and customisation. The introduction of the Ethereum Vault Connector (EVC) further enhances interoperability, enabling vaults to connect and interact with one another. This innovation facilitates cross-collateralisation and composable lending strategies across different vaults, expanding the design space for both users and developers. Vault creators can choose from a wide range of collateral types, including ERC-20 tokens, NFTs, and synthetic assets, while also customising features such as hook design, profit and loss simulators, custom limit orders and strategy vaults tailored to specific use cases. This modular architecture has significantly enhanced Euler’s flexibility and utility, attracting notable integrations with protocols such as Usual, Sonic, and Pendle, which have contributed to the rapid growth of Euler V2’s TVL.

The EUL token plays a central role in the new ecosystem. It is used as the bidding currency in auctions for the fees generated by Euler Vaults. Proceeds from these auctions are directed to the protocol treasury, where they can be allocated to various initiatives that further support and enhance the ecosystem.

Real-World Asset Innovator: Maple Finance

Maple Finance TVL

Maple Finance, once facing existential challenges, has emerged as a leader in Real-World Asset (RWA) lending innovation. RWAs have become a focal point in DeFi, heralded for their potential to onboard traditional financial instruments onto blockchain infrastructure. The benefits are clear: instant settlement, reduced reliance on intermediaries, lower costs, enhanced accessibility, expanded collateral options, and 24/7 market availability. However, not every financial product is suited for on-chain deployment, particularly unsecured loans, which remain a significant challenge. In December 2022, Maple Finance faced its most severe test when Orthogonal Trading defaulted on its loans, a direct fallout from the FTX collapse. This event exposed the vulnerabilities of off-chain credit risk management and dealt a heavy blow to Maple’s reputation. In response, the Maple team took decisive action by assuming direct oversight of loan origination and management through the launch of Maple Direct, bringing a more hands-on and transparent approach to its credit operations.

Having steadily regained investor confidence, Maple expanded its offering by launching Syrup, a platform designed to democratise institutional yield opportunities and make them accessible to the broader DeFi community. Syrup’s structure bears similarities to leading RWA platforms such as Ondo Finance and Flux Finance, but with Maple’s distinct focus on transparent on-chain credit management. The team’s innovation didn’t stop there. Shortly after Syrup’s debut, Maple introduced its Lend + Long Pool, a novel product that channels yield generated from loan portfolios into Bitcoin call options. This structure provides lenders with potential upside exposure to Bitcoin, while maintaining capital preservation on their principal, effectively blending traditional credit yields with crypto-native growth opportunities.

Maple’s efforts to align with institutional standards have yielded significant partnerships, including the onboarding of Bitwise, a prominent asset manager with over $12 billion in assets under management. Bitwise utilises Maple’s on-chain credit infrastructure while maintaining compliance with stringent institutional regulatory requirements. The team also joint-collaborated with Ethena to be one of the first 5 protocols that are integrating the new Converge blockchain. These collaborations are the testaments to Maple’s maturation and credibility in the RWA space.

As part of its commitment to delivering real value to participants, Maple introduced MIP-13, a proposal that directs 20% of protocol fee revenues toward the buyback of SYRUP tokens on the open market. These tokens are then redistributed to SYRUP stakers on a monthly basis, reinforcing the protocol’s alignment with its community and incentivising long-term participation.

39x Capital Efficiency and Sustainable Yield: Fluid

Fluid DEX Marketshare on Ethereum

In the competitive landscape of DeFi lending and trading, capital efficiency is critical to delivering sustainable, attractive real yields for lenders. Fluid Finance has emerged as a leader in this domain, leveraging an innovative dual-purpose architecture that maximises the utility of user assets. By enabling deposited assets to simultaneously provide trading liquidity and be available for borrowing, Fluid effectively 39x capital efficiency, creating a system where capital works harder on both sides of the market.

For lenders, Fluid introduces Smart Collateral, where deposited assets are in pairs such as wstETH/ETH, and serve as a concentrated liquidity position managed by Fluid. This allows lenders to earn swap fees on top of lending fees. For borrowers, Fluid introduces Smart Debt, where borrowed assets continue to facilitate trading liquidity and generate liquidity yield. This yield is automatically applied to reduce outstanding debt over time, offering borrowers a self-repaying mechanism while maintaining exposure to trading opportunities. As a result, using a vault with wstETH/ETH as Smart Collateral and Smart Debt at a 95% LTV, users can get maximum 20x leverage on collateral and 19x leverage on debt, effectively 39x capital efficiency.

The ETH/USDC trading pair exemplifies the protocol’s efficiency, consistently generating the highest trading volumes on Fluid’s platform. Smart collateral depositors in this pair are earning double-digit APYs, while borrowers benefit from self-repaying loans tied to the liquidity yield. This model is made possible by Fluid’s integrated design, which maximises asset utilisation without compromising liquidity or capital security.

Despite managing under $700 million in total deposits, Fluid DEX commands an impressive 16% market share of Ethereum’s spot trading volume, second only to Uniswap. This rapid growth trajectory continues to accelerate, with further multi-chain expansion planned to solidify Fluid’s position as the ultra-capital-efficient protocol in DeFi. Fluid’s business model translates capital efficiency into tangible value. The protocol has already achieved $5.1 million in annualised revenue and is on track to meet its target of $10 million. Upon reaching this milestone, Fluid will activate a strategic buyback program, allocating 100% of protocol revenue toward purchasing Fluid tokens from the open market. This initiative directly aligns token holder incentives with protocol growth, ensuring long-term value accrual for the community. Despite launching its smart lending product less than five months ago, Fluid has generated $756,944 in revenue in February 2025 alone. This early success underscores the growing demand for Fluid’s capital-efficient model.

Looking ahead, the team has teased the upcoming launch of Fluid DEX V2 in 2025, which aims to capture over 50% of Ethereum’s trading volume. The expansion roadmap includes entry into the perpetuals and Real-World Assets (RWA) markets, further diversifying Fluid’s product suite and reinforcing its status as a next-generation DeFi infrastructure.

Ultra Liquidation Engine on Solana: Kamino Finance

Real-Time Liquidation Analysis on SOL Price Shock

Lending protocols are no longer confined to Ethereum or its Layer 2 ecosystems. Across alternative Layer 1 blockchains, dominant protocols are emerging. Kamino Finance has firmly established itself as the market leader on Solana. Kamino currently commands an impressive 85.4% share of Solana’s lending market, setting a new standard for capital efficiency and risk management within the ecosystem.

Kamino’s journey began as an automated rebalancing platform for Concentrated Liquidity Market Maker (CLMM) liquidity providers. Leveraging that success, Kamino quickly expanded into DeFi lending, offering an array of intuitive and capital-efficient products designed to cater to both novice and advanced users. These include:

-

One-click looping strategies for leveraged exposure

-

Leverage long/short positions

-

eMode for highly correlated assets, enabling enhanced capital efficiency

-

Poly-Linear Interest Rate Curve, which dynamically adjusts rates based on utilisation, minimising system shocks

-

Support for CLMM LP tokens as collateral, unlocking additional liquidity for LP participants

Kamino’s seamless user interface (UI) and comprehensive portfolio management tools have also been key differentiators. Users can effortlessly track their positions, manage risk, and monitor real-time profit and loss (PnL), making sophisticated strategies accessible to a broader audience. Kamino has capitalised on Solana’s rapidly growing ecosystem by integrating with major projects and assets. The protocol offers multiply strategies for Sanctum-based Liquid Staking Tokens (LSTs), PayPal USD (PYUSD), and Jupiter LP tokens (JLP), facilitating broader access to leverage and liquidity within Solana’s high-growth sectors.

A cornerstone of Kamino’s success lies in its robust risk management framework, designed to protect users and preserve protocol stability. Kamino employs an auto-deleveraging mechanism, which gradually liquidates collateral with a minor penalty that escalates over time, up to a maximum of 10%. This Ultra Liquidation Engine helps mitigate cascading liquidations and reduces the risk of system-wide insolvency. Kamino also categorises assets into distinct risk tiers, determining whether they qualify as Isolated Debt, Isolated Collateral, or Dual-Purpose Assets. Borrow Factors are assigned to each asset, defining their respective borrowing capacities and ensuring prudent capital allocation. Further enhancing its protective measures, Kamino incorporates a hybrid pricing mechanism, combining Exponentially Weighted Moving Averages (EWMA) with Time-Weighted Average Prices (TWAP). This safeguards the protocol against oracle manipulation and flash loan attacks, ensuring fair and accurate asset valuations.

Despite recent market volatility, Kamino has demonstrated exceptional resilience, recording zero bad debt. This performance underscores the effectiveness of its risk controls and liquidation mechanisms, cementing its reputation as a secure and efficient lending protocol within the Solana ecosystem.

Quick Table Comparison

According to the data presented in the table above, both MORPHO and KMNO have significant upcoming token unlocks still on the horizon. In contrast, SYRUP holders remain highly engaged, with strong participation in staking activities. Over the past 365 days, Aave and Morpho have demonstrated robust growth in borrowing demand within the lending sector. Meanwhile, Liquity continues to lag behind, primarily due to delays in the launch of its V2 upgrade. Additionally, borrowing demand on Solana has grown at a slower pace compared to EVM-compatible ecosystems. Notably, Euler, Maple, and Fluid have exhibited exceptional growth, with Euler standing out for its continued expansion over the past 30 days, despite an overall slowdown in borrowing demand across the market.

Both Euler and Fluid are ushering in a new era of hyper-capital efficiency, with utilisation rates consistently exceeding 40%. It’s important to note that utilisation rates in this analysis are calculated using the ratio of TB to TD for simplicity. This may differ from other methodologies, which often define utilisation as total borrows divided by available supply.

Blue-chip protocols such as Aave and Kamino continue to display strong FDV/TB ratios. However, Euler also maintains a relatively low ratio, reflecting its current phase of high growth. Among the protocols analysed, only Morpho and Kamino have yet to implement mechanisms for value accrual. Similarly, when evaluating FDV/Fees ratios, Euler and Fluid stand out alongside established protocols like Aave and Kamino, maintaining relatively low ratios that suggest attractive valuations relative to their fee generation. Fee and revenue figures are derived from protocol activity over the past 30 days and annualised to provide a standardised view of potential yearly performance. In terms of revenue margins, Liquity’s stablecoin operations deliver the highest profitability across all protocols. Among general lending protocols, Kamino achieves the strongest revenue margins, highlighting its operational efficiency within the sector.

Lending Protocols as The Beta Play on Alternative Layer-1s

Lending protocols often serve as high-beta investment opportunities for gaining exposure to the growth of emerging blockchain ecosystems. As core infrastructure, these protocols typically benefit from increased network activity and liquidity inflows. Examples include Silo Finance on Sonic, Dolomite on Berachain, HypurrFi on HyperEVM, Suilend on Sui, Venus on BNB Chain, JustLend on Tron, Yei Finance on Sei, Aries Markets on Aptos, Benqi on Avalanche, and Rhea Finance on NEAR. These platforms are strategically positioned to capitalise on their respective networks' traction and ecosystem expansion.

However, the attractiveness of these opportunities depends on the tokenomics of each lending protocol. In particular, protocols with low emission rates and a high circulating supply tend to offer more sustainable value accrual for token holders, reducing the risks associated with inflationary pressure and excessive dilution.

Summary

The lending market continues to evolve and expand at an exponential pace, driven by increasingly permissionless frameworks and chain-agnostic approaches. Enhanced customisability within lending protocols is fostering greater integration by other decentralised applications (dApps), while innovations in capital efficiency are fuelling organic demand. This, in turn, enables lending protocols to offer sustainable and attractive yields to both lenders and borrowers.

As foundational pillars of the DeFi ecosystem, lending protocols play a critical role in supporting the broader growth of the blockchain sector. Their expansion is intrinsically linked to the dynamics of market speculation, an enduring aspect of human behaviour, which amplifies the demand for leveraged borrowing. Additionally, lending protocols benefit from the rising on-chain supply of stablecoins, as investors seek yield opportunities in DeFi, engage in delta-neutral strategies, or hold capital in reserve for emerging market opportunities. With growing awareness that memecoin trading is often structured against retail investors, market attention is gradually shifting toward tokens with tangible value propositions. Investors are increasingly prioritising assets that generate revenue, have high circulation, and offer direct value accrual to token holders—criteria that lending protocols consistently meet.

Reference

Contact ChainUp Investment

Please Select

Remarks

0/200

Trending topics

1

Weekly Market Insight: March Week 4

2

Weekly Market Insight: March Week 3

3

Weekly Market Insight: March Week 2

4

Weekly Market Insight: February Week 4

5

Weekly Market Insight: January Week 3

6

Weekly Market Insight: January Week 1

7

Weekly Market Insight: December Week 4

8

Weekly Market Insight: December Week 2

9

Weekly Market Insight: December Week 1

10

Understanding The DePIN Economics