As the world shifts towards an increasingly digital economy, the financial industry is undergoing significant transformations. Among the most promising developments in this evolution is the rise of Central Bank Digital Currencies (CBDCs). These digital currencies, issued and regulated by central banks, offer governments and financial institutions powerful tools to modernize payment systems, ensure financial stability, and promote financial inclusion. Recently, the UK launched its own CBDC, the Digital Pound, marking a significant step in the country’s digital finance transformation

The Transformative Impact of CBDCs on Finance

The mass adoption of CBDCs could profoundly change the financial landscape. By providing unbanked populations with access to secure financial services, CBDCs enhance financial inclusion and simplify everyday transactions. Additionally, they streamline operations, significantly reducing transaction costs for both domestic and international payments.

One of their most significant benefits lies in their ability to facilitate faster and cheaper international payments, addressing a major challenge in global finance today. CBDCs also provide central banks with real-time transactional data, enhancing their stability to monitor economic activity and adjust monetary policy more swiftly and accurately. This improved data flow allows for quicker responses to economic shifts, reducing lag in policy implementation and fostering greater economic stability. Furthermore, by reducing reliance on private digital currencies, CBDCs enhance financial stability, making them a cornerstone of a resilient digital financial system.

This transformative potential makes CBDCs a pivotal component of modern finance, but how do they compare to other digital assets like stablecoins and cryptocurrencies? Understanding these distinctions is crucial to appreciating the unique role of CBDCs in reshaping financial systems.

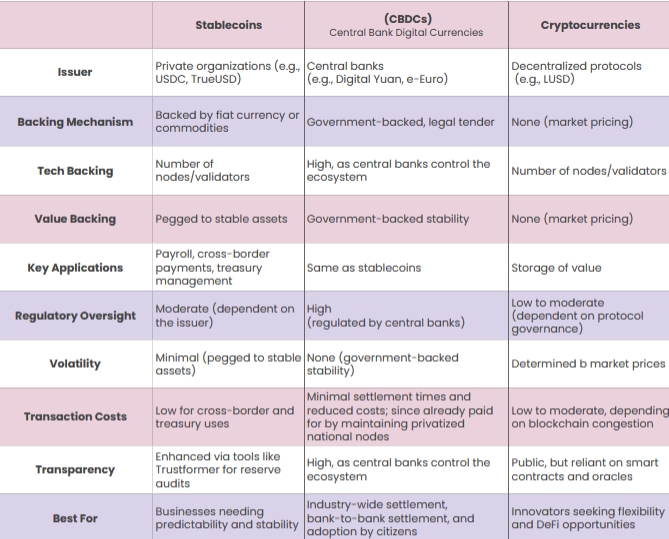

CBDC vs. Stablecoins and Cryptocurrencies: What Sets Them Apart?

CBDCs are often compared to other digital assets like stablecoins and cryptocurrencies, but their design and purpose differ significantly. Unlike cryptocurrencies, which operate on decentralized systems and lack intrinsic backing, CBDCs are centralized and backed by governments, ensuring stability and trust.

Similarly, while stablecoins are pegged to fiat currencies or assets, they are privately issued and carry counterparty risks. CBDCs stand apart due to their robust regulatory oversight, which positions them as secure and efficient tools for modernizing financial systems.

While CBDCs focus on secure and efficient payments, stablecoins are primarily used in decentralized finance (DeFi), and cryptocurrencies function as decentralized payment methods. The strong regulatory oversight of CBDCs further distinguishes them, positioning them as a cornerstone for the future financial system.

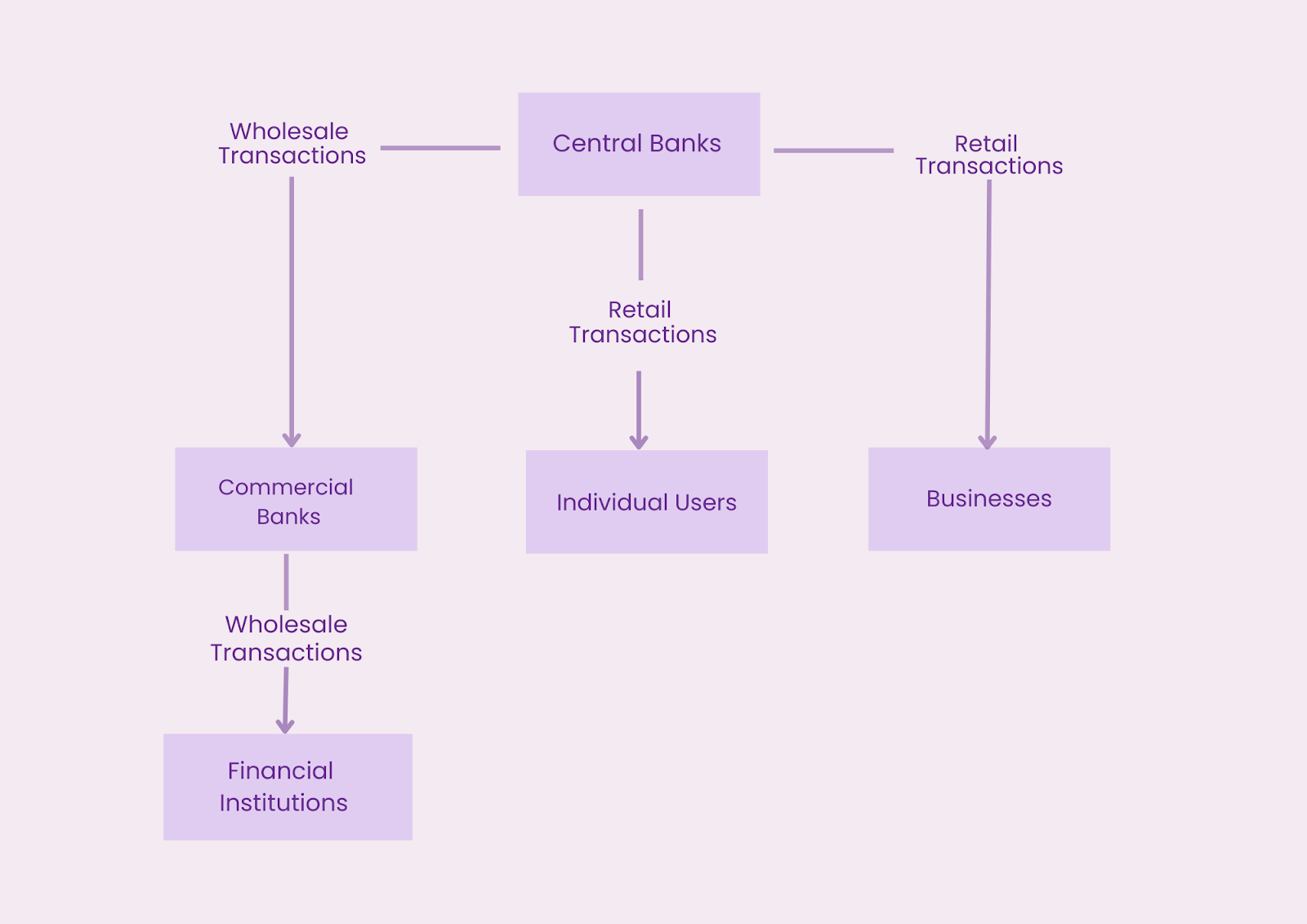

Recognizing these distinctions, it’s essential to delve deeper into how CBDCs function in practice. Their design allows for specific applications tailored to both institutional and public needs, demonstrating their flexibility in addressing diverse economic challenges. This leads to the categorization of CBDCs into wholesale and retail types, each with unique purposes and benefits.

Wholesale vs. Retail CBDCs: Key Applications and Benefits

CBDCs are categorized into two main types:

-

Wholesale CBDCs are designed for financial institutions to enable secure and efficient interbank settlements, streamline large-value transactions, and reduce operational costs.

-

Retail CBDCs aim at the general public for everyday transactions, acting as a digital equivalent of cash. They enhance financial inclusion, simplify payments, and provide secure financial services for unbanked populations.

These applications showcase the flexibility of CBDCs in addressing diverse economic and financial needs.

The ability of CBDCs to address both institutional and public needs has made them a pivotal element in financial modernization. As central banks worldwide recognize the benefits of wholesale and retail CBDCs, the race to implement these digital currencies has intensified.

The race to implement CBDCs is driven by competition from private innovations like stablecoins and DeFi. Central banks seek to preserve monetary sovereignty and ensure their currencies stay relevant by offering secure, state-backed alternatives that safeguard financial stability.

Across the globe, numerous countries are exploring, piloting, and even launching CBDC initiatives to harness their potential for improving cross-border payments, financial inclusion, and national economic stability.

Let’s explore the global landscape of CBDC development and see how different regions are driving innovation in digital finance.

The Global Race to Implement CBDCs: Regional Updates and Insights

Numerous countries worldwide are actively exploring and developing CBDCs. Some have even launched pilot programs or full-scale implementations. This global effort underscores the growing recognition of the potential benefits of CBDCs in modernizing payment systems and fostering financial innovation.

Regional CBDC Updates: HK, CN, SG, EU, US, UK

In Hong Kong, the Hong Kong Monetary Authority (HKMA) is making significant strides in the development of the e-HKD. The authority is placing a strong emphasis on ensuring the e-HKD’s interoperability with existing payment systems and exploring its potential for cross-border use cases. Meanwhile, China is leading the charge in CBDC development, having rolled out extensive pilot programs for its digital yuan (e-CNY). The country is actively investigating its application in both retail and wholesale transactions, positioning itself as a pioneer in the global CBDC race.

Singapore is also advancing its CBDC plans with the Monetary Authority of Singapore (MAS) studying various models, focusing on improving the efficiency of cross-border payments. In Europe, the European Central Bank (ECB) is making headway with the digital euro, which aims to provide citizens and businesses across the Eurozone with a digital currency that simplifies cross-border transactions. In the United States, the Federal Reserve is researching the potential benefits and risks of a U.S. CBDC, particularly its implications for monetary policy and financial stability.

Notably, the United Kingdom has made headlines with the recent announcement of the Digital Pound. The Bank of England (BoE) is set to launch this initiative in 2025, operating as a sandbox environment to experiment with CBDC APIs, test innovative use cases, and evaluate potential business models.

According to the BoE’s progress report, the lab will serve as a platform for collaboration with private sector partners, aiming to address payment system challenges and drive technological innovation. Stakeholder engagement will remain a priority, with insights gained from working groups, surveys, and experiments helping shape the digital pound’s design phase.

This initiative reflects the UK's commitment to leading innovation in digital finance, alongside other global leaders in the CBDC race.

Each of these regions is driving forward the development of CBDCs at different paces, but all recognize the importance of digital currencies for modernizing financial systems and enhancing cross-border payments. This global effort reflects how integral CBDCs are to the future of finance.

As earlier discussed, policymakers around the world have implemented and begun to create frameworks that ensure regulatory clarity and stability for CBDCs. Such as in the UK, China, Singapore, US and the European Union. By addressing these challenges head-on, central banks and future regulations can ensure the seamless integration of CBDCs into the global financial ecosystem, fostering trust and stability.

Embracing the CBDC Revolution: What Lies Ahead

The development of CBDCs marks a significant leap toward a more efficient, inclusive, and resilient financial future. Addressing challenges through innovation and collaboration can unlock the transformative potential of CBDCs in digital finance.

Stay informed on the latest CBDC developments and how they’re shaping the future of finance.

Ready to Harness the Future of Finance with ISO-Certified Cryptocurrency Solutions?

At ChainUp, we don’t just follow the trends—we empower businesses to lead the transformation. With ISO-certified blockchain solutions, we ensure the highest levels of security, compliance, and reliability as you embrace the future of finance with Central Bank Digital Currencies (CBDCs).

As CBDCs revolutionize the global financial landscape, now is the time to explore how this innovation can drive efficiency, inclusion, and growth in your organization. Whether you’re looking to:

-

Integrate CBDC-ready payment systems

-

Streamline cross-border transactions

-

Enhance operational efficiency with secure blockchain systems

Our ISO-certified solutions provide the trust and scalability you need to stay ahead in the evolving digital finance ecosystem.

Get Started Today

Be part of the CBDC revolution. Let us help you build the foundation for a resilient, future-proof financial ecosystem. Explore options with ChainUp.